How to Save on Employee Benefits: The Tax Implications of FBT & PAYE Explained

An overview of the process, tax implications, and the true value of distributing fringe benefits over cash allowances to employees.

.png)

Attractive employee benefits packages have evolved from a nice-to-have to a fundamental pillar of a successful Employee Value Proposition (EVP). These packages are geared toward attracting and retaining talent while creating a noteworthy differentiator for standout ‘people-centric’ employers and organisations.

New Zealand companies have two primary avenues for distributing benefits: cash allowances subject to PAYE and fringe benefits. When distributed strategically, fringe benefits can result in employer cost savings while maximising the benefit for employees. Yet many companies miss out on potential tax savings yearly by not clearly understanding which options are the most cost-effective while complying with NZ tax laws and Inland Revenue requirements.

This article provides an overview of the process, tax implications, and the true value of distributing fringe benefits over cash allowances to employees. It illustrates why many organisations choose to offer certain fringe benefits and use Extraordinary’s centralised benefits card and platform to do so, helping improve their bottom line and EVP.

PAYE vs FBT: Recap and Tax Implications

To understand how fringe benefits can be used to your tax advantage, let’s recap the two primary tax systems that can be applied when providing benefits to employees:

1. PAYE

Pay As You Earn (PAYE) is the system by which income tax and any other IRD-related employee obligations (including the ACC levy, KiwiSaver and Student Loan repayments) are deducted directly from your employee’s salary or wages and paid to Inland Revenue on the employee's behalf. This occurs through your payroll system. The employee is left with a lower post-tax sum in their bank account each pay period, but these regular contributions help them meet their tax obligations in a simple way. This helps avoid employees getting into difficult situations when it’s time to file a personal tax return. Employers must pay additional Kiwisaver contributions of at least 3% on all pre-tax values as part of their Kiwisaver obligations for all employees involved in the scheme.

Receiving a cash benefit

When an employer distributes a benefit as a cash allowance, it is added to the employee’s wages and subject to PAYE tax deductions. This means the employee is left with less money to spend after their income tax is deducted, they may be pushed into a higher tax bracket, and they will also have Kiwisaver and ACC levies deducted from the allowance. The employer also pays additional Kiwisaver fees.

2. FBT

A fringe benefit is a non-cash perk that an employee receives from their employer. Common fringe benefits include gift cards, health perks like gym memberships or wellness allowances, and company cars that can be taken home and used outside work hours.

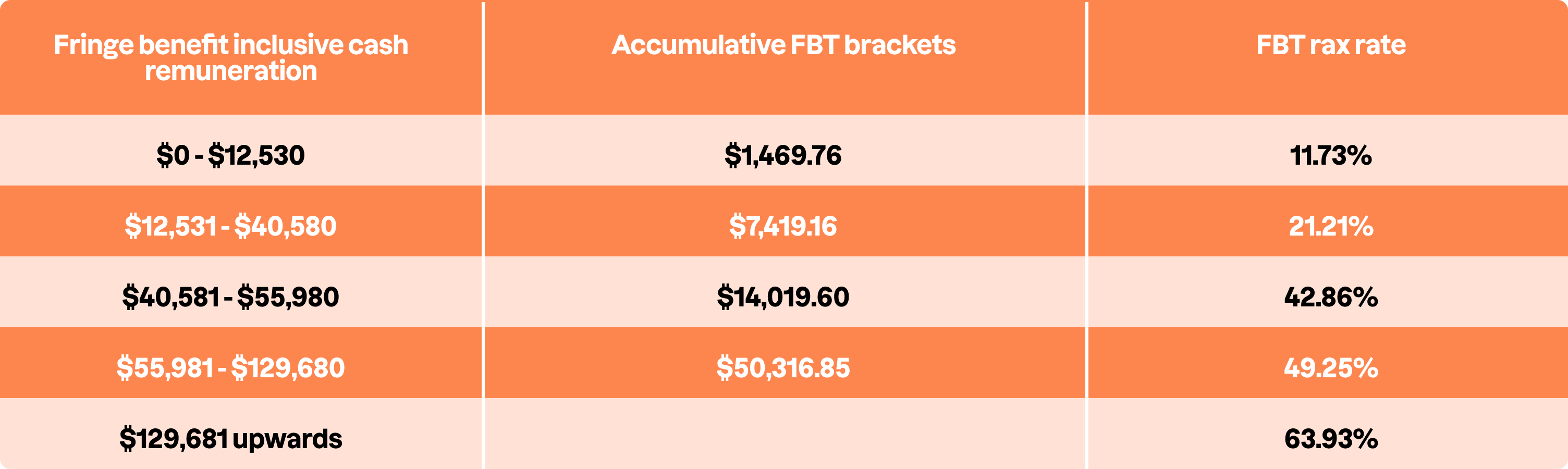

Fringe Benefits Tax (FBT) is the tax employers are responsible for paying on these benefits. FBT is calculated and remitted based on the taxable value of the benefits. The tax rates vary depending on the employee's position (employee vs. shareholder-employee) and whether you choose to use the flat rate or the alternate rate calculation, which factors in an employee’s individual income and sees a lower FBT rate applied to lower-income earners.

While the alternate rate methodology sees lower FBT obligations for the lower tax brackets, a significant deterrent to applying the alternate rate is the individual itemised reporting and calculations required for every employee, a traditionally laboursome administrative task. This is where platforms like Extraordinary have streamlined the process to simplify it for companies, providing an itemised breakdown per employee for any given period, at any time. As such, distributing benefits as fringe benefits as opposed to cash allowances subject to PAYE can become more favourable for certain benefits and circumstances.

Regardless of how benefits are delivered, they must be accurately recorded and reported so that tax can be applied.

Comparative Analysis: FBT vs PAYE

Here are some illustrative scenarios to help you better understand how New Zealand employers reduce costs and improve tax efficiency by offering non-cash benefits on their Extraordinary card (subject to FBT) instead of cash allowances (subject to PAYE). Under FBT, the total cost to the employer for their employees to access these talent-retaining benefits is lower in many cases.

Scenario One: Relocation Costs

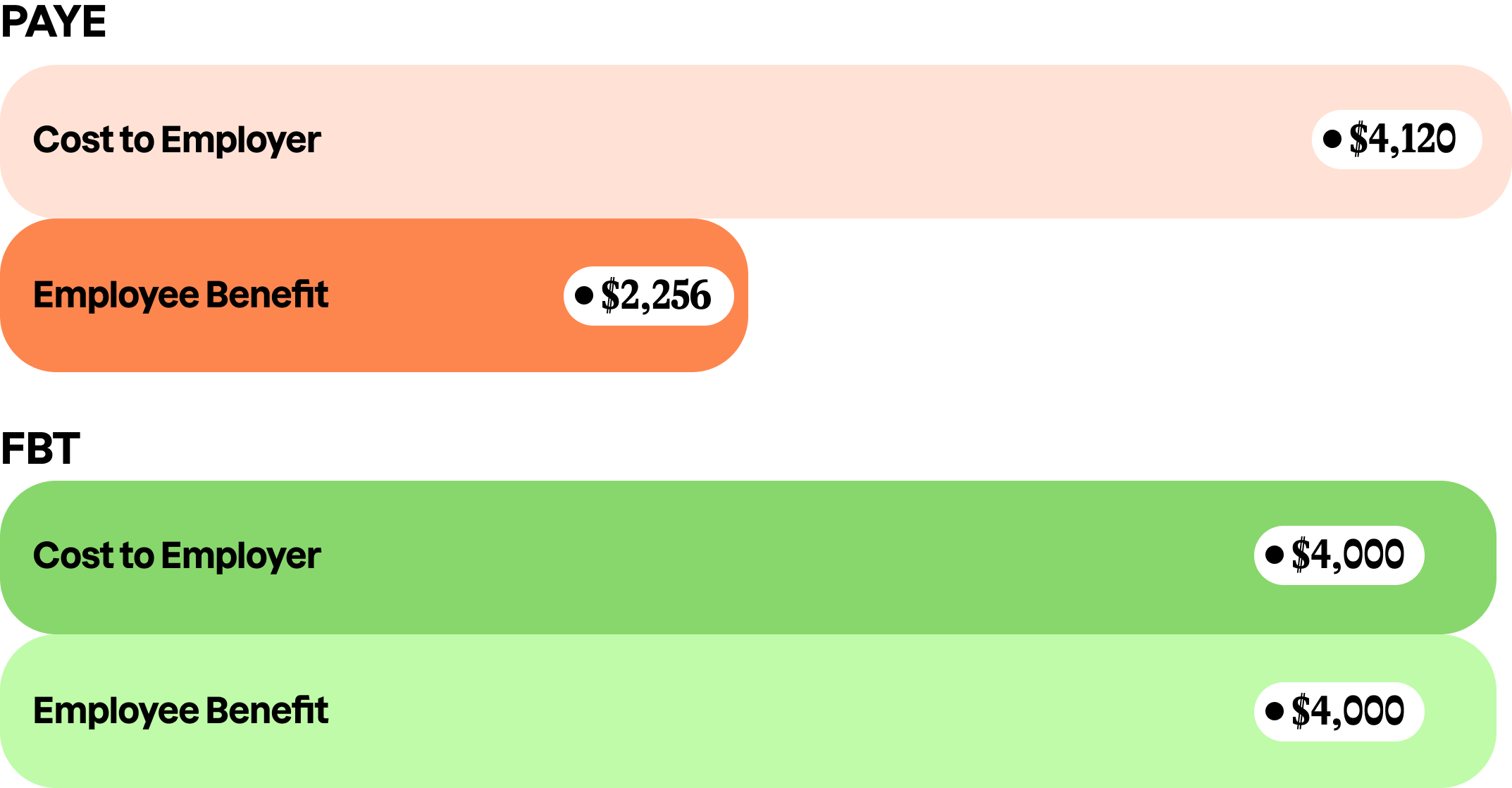

Roger’s Building Solutions has set up a new office in a new city, and Geoff and Janine must relocate as a mandatory part of their role. Geoff and Janine each earn $180,000 per annum and are allocated $4,000 to help with relocation costs. The employer has two choices:

- Provide $4,000 paid as cash paid into the next pay cycle to be spent on relocation costs.

- Load $4,000 onto the employee’s Extraordinary card in a dedicated account for relocation expenses. The card functions like a Mastercard and is accepted in the same places.

Here are the financial implications of both scenarios:

1. Geoff receives the $4,000 cash allowance in his next pay packet. Cash allowances are attributed to earnings and are taxed under PAYE. Geoff’s taxable income becomes $184,000. Geoff must pay income tax, ACC levies and deduct Kiwisaver from his relocation allowance. After these are deducted, he has $2,256.00 for relocation costs. Roger’s Building Solutions must also contribute an additional $120 in KiwiSaver contributions (which he cannot immediately access).

2. Janine receives the $4,000 as a fringe benefit on her Extraordinary card, exclusively for relocation costs. Janine’s taxable income stays at $180,000. She does not pay income tax, ACC levies or KiwiSaver on her relocation benefit. Janine also retains the full $4,000.00 on her Extraordinary card to cover much more of her relocation costs. As mandatory relocation costs are exempt from FBT, Roger’s Building Solutions is not required to pay FBT for the $4,000. They can deliver the full value of the benefit to Janine and save another $120 in KiwiSaver fees that they would have needed to pay had they gone through PAYE.

Scenario Two: Gift Card vs Cash Allowance

Roger’s Building Solutions provides every employee with a $500 gift bonus for Christmas, including Mandy and Liam. To ensure that both employees are left with $500 available to spend after any tax deductions, Roger’s has two choices:

- Provide the $500 as a cash allowance

- Provide the $500 as a fringe benefit for gifts on their Extraordinary card

Both methods have tax implications: the cash allowance is subject to PAYE, and the fringe benefit is subject to FBT. In this case, using the Extraordinary card results in cost savings for Roger’s Building Solution. Just type the ‘500’ value into our FBT vs PAYE calculator below to see how much a $500 gift bonus really costs an employer (per employee) under each tax system and relative to the employee’s tax bracket.

Scenario Three: Transport Benefit

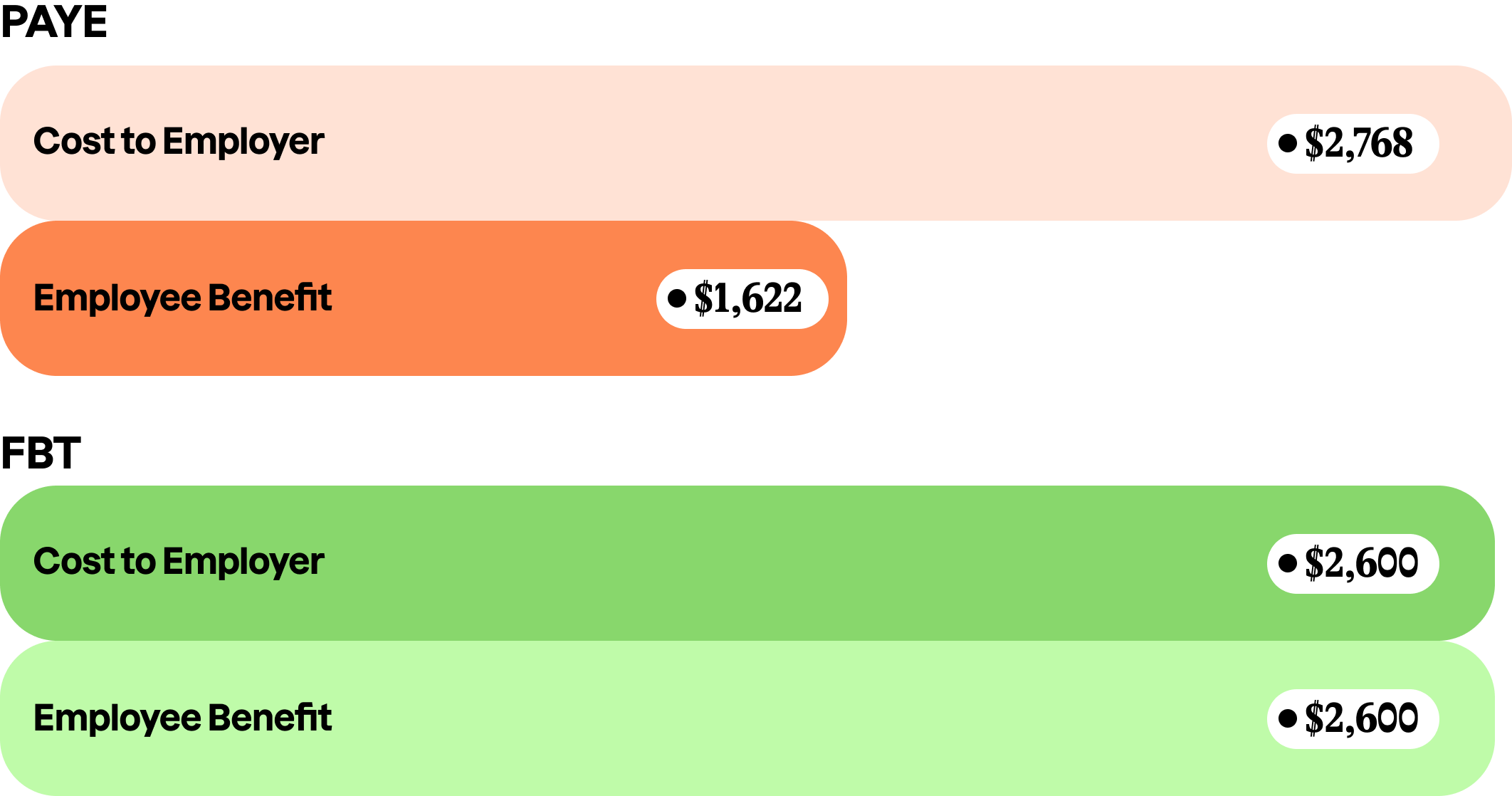

Jessica and Matthew work at Roger’s Building Solutions in the CBD and commute to and from work via bus. They both earn $70,000 per annum. Roger’s wants to contribute towards their commuting costs, which cost Matthew and Jessica $2,600 annually. Roger’s has two choices:

- Provide a $2,600 transport cash allowance annually

- Provide a $2,600 public transport benefit on their Extraordinary card, approved for use only for public transport fees.

Here are the financial implications of both scenarios:

1. Jessica receives the $2,600 cash allowance for transport costs. Cash allowances are attributed to earnings and are taxed under PAYE. Her taxable income becomes $72,600. She must pay income tax, ACC levies and deduct Kiwisaver from her transport allowance. After these are deducted, she has $1,622.40 to spend on bus fares, leaving her $977.60 out of pocket each year. Roger’s must also contribute an additional $78 in KiwiSaver costs.

2. Matthew receives $2,600 as a fringe benefit on his Extraordinary card. It is designated solely to the public transport category, making it exempt from FBT under section CX 19C of the Income Tax Act 2007. Matthew’s taxable income stays at $70,000. He does not pay income tax, ACC levies or KiwiSaver on his transport benefit. Matthew retains the full $2,600.00 on his Extraordinary card to use for public transport. He never has to pay out of pocket for his transport, and Roger’s Building Solutions is able to deliver the full value of their benefit while saving $78 in additional Kiwisaver fees.

Employee Benefits: Common Mistakes to Avoid

When dealing with employee benefits and allowances, avoid these (potentially costly) pitfalls:

- Inadequate record-keeping for FBT compliance - employers must maintain detailed and accurate records of all fringe benefits to ensure compliance and avoid IRD penalties. Extraordinary helps by providing an itemised breakdown of all expenditures and benefit allocations per employee, reducing the risk of oversights or confusion.

- Misclassifying cash allowances as fringe benefits - cash allowances are subject to PAYE deductions, not FBT, and must be processed accordingly in payroll.

- Overcomplicating payroll with excessive allowances - structuring remuneration with multiple small allowances increases administrative complexity and compliance risks.

- Failing to correctly apportion personal vs. business use - benefits such as company vehicles must have proper documentation (e.g. logbooks) to determine taxable portions accurately.

- Overlooking tax-efficient compensation strategies - employers may reduce tax liabilities by offering FBT-exempt benefits, such as work-related training or public transport subsidies, instead of taxable allowances.

- Incorrectly assuming certain benefits are tax exempt - some employer-provided benefits, such as home internet reimbursements, may be subject to FBT unless they meet exemption criteria under IRD regulations.

Extraordinary Supports Companies To Leverage FBT Efficiently

Efficiently processing your fringe benefits and staying tax-compliant can be complicated and time-consuming if you don’t have the right systems in place. Benefits and allowances need to be well-tracked and managed to avoid unnecessary expenses and administrative burdens. Extraordinary’s streamlined platform and benefits card is trusted by both large national companies and Australasia’s major financial institutions.

By using a centralised payment card, organisations can seamlessly distribute allowances, benefits, recognitions and gifts while gaining enhanced visibility and control over all FBT-reportable expenses as well as all non-payroll payments beyond what we have illustrated in this article. Extraordinary removes the complexity of managing multiple reimbursement claims and manual expense tracking while giving employees a physical benefit-loaded card where they get to see and use the full sum of their benefits without it being ‘lost’ in standard household outgoings like with a regular pay packet.

With Extraordinary, you get:

- Seamless benefits distribution. We allow organisations to distribute a wide range of taxable and non-taxable benefits, including:

- Employee gifts, recognition, and rewards

- Fuel allowances

- Health and wellness benefits

- Meal allowances

- Public transport subsidies

- Centralised FBT tracking and reporting - Extraordinary offers a new level of visibility into fringe benefit taxable expenses by automatically capturing and categorising transactions. We replace the need to manually input benefit allocations into spreadsheets or systems, allowing our partners to easily generate and export reports that reflect aggregated spend amounts per employee within a filing period. This significantly simplifies the FBT filing process.

- A clear insight into cost efficiencies that may otherwise be difficult to detect due to a lack of proper visibility of benefits, spending, or improperly categorised transactions. The detailed transactional data provided allows employers to identify and apply exemptions where appropriate more easily. A common example is for public transport under section CX19C of the Income Tax Act, where certain public transport benefits are FBT-exempt, but must be properly tracked, allocated and reported to be claimed.

Why Leading Companies Choose Extraordinary

- Employees feel more valued by having an uncomplicated, easy-to-use benefits card, and it offers greater freedom and choice in how they access their benefits.

- Employees enjoy the full value of their benefits, making it go further, which can make a big difference when it comes to benefits like health and wellness perks.

- Employers also benefit when employees can clearly attribute the reward they receive to the company providing it, which is more likely when a specific benefit is available on a dedicated card than a general cash benefit that disappears into the mix of their household expense account.

- Time and cost-saving transparency and reporting - both employers and employees gain real-time insight into how benefits are used, ensuring accurate tracking for reliable reporting and filing, and allowing the insights to help the company make informed decisions in their best interest.

- Centralising a company’s benefit distribution and automating FBT tracking means administrative overheads are able to be significantly reduced, compliance risks minimised, and tax efficiencies maximised.

- Well-managed benefits programs play a strong role in staff satisfaction, retention, and overall workplace morale.

Key Takeaways:

- In many situations, offering employee benefits (as fringe benefits) in place of cash allowances can result in cost savings for both parties, elevating the true value of the funds allocated by the employer.

- Distributing and allocating benefits is no longer administratively tedious due to platforms like Extraordinary that do the heavy lifting for you, allocating benefits and expenses appropriately so companies can make the most of the available tax advantages

- Employees can benefit greatly from well-allocated benefits, both financially and psychologically. Read more about how employee benefits can drive employee behaviour here.

Partnering with New Zealand’s leading benefits solution is easier than ever. Get started by connecting with one of our team members, who will go through everything you need to know about how Extraordinary can help you centralise and get on top of your non-payroll payments while helping improve your tax efficiency, bottom line, employee satisfaction and more.

Disclaimer

The information in this article is for general informational purposes only and does not constitute tax, financial, or legal advice. While we strive for accuracy, tax laws and regulations in New Zealand may change over time. The content provided is based on publicly available information and should not be relied upon as a substitute for professional tax advice.

Before making any tax-related decisions, we strongly recommend consulting a qualified accountant, tax professional, or the Inland Revenue Department (IRD) for guidance specific to your situation. The author and publisher disclaim any liability for actions taken based on the information provided in this article.

Useful Resources

Related Resources

Strengthening Ways of Working Through Recognition

Infographic: Pre-Tax Public Transport

.jpeg)